How much of a tax credit do you get per child

The Child Tax Credit | The White House

To search this site, enter a search termThe Child Tax Credit in the American Rescue Plan provides the largest Child Tax Credit ever and historic relief to the most working families ever – and as of July 15th, most families are automatically receiving monthly payments of $250 or $300 per child without having to take any action. The Child Tax Credit will help all families succeed.

The American Rescue Plan increased the Child Tax Credit from $2,000 per child to $3,000 per child for children over the age of six and from $2,000 to $3,600 for children under the age of six, and raised the age limit from 16 to 17. All working families will get the full credit if they make up to $150,000 for a couple or $112,500 for a family with a single parent (also called Head of Household).

Major tax relief for nearly

all working families:

$3,000 to $3,600 per child for nearly all working families

The Child Tax Credit in the American Rescue Plan provides the largest child tax credit ever and historic relief to the most working families ever.

Automatic monthly payments for nearly all working families

If you’ve filed tax returns for 2019 or 2020, or if you signed up to receive a stimulus check from the Internal Revenue Service, you will get this tax relief automatically. You do not need to sign up or take any action.

President Biden’s Build Back Better agenda calls for extending this tax relief for years and years

The new Child Tax Credit enacted in the American Rescue Plan is only for 2021. That is why President Biden strongly believes that we should extend the new Child Tax Credit for years and years to come. That’s what he proposes in his Build Back Better Agenda.

Easy sign up for low-income families to reduce child poverty

If you don’t make enough to be required to file taxes, you can still get benefits.

The Administration collaborated with a non-profit, Code for America, who created a non-filer sign-up tool that is easy to use on a mobile phone and also available in Spanish. The deadline to sign up for monthly Child Tax Credit payments this year was November 15. If you are eligible for the Child Tax Credit but did not sign up for monthly payments by the November 15 deadline, you can still claim the full credit of up to $3,600 per child by filing your taxes next year.

The deadline to sign up for monthly Child Tax Credit payments this year was November 15. If you are eligible for the Child Tax Credit but did not sign up for monthly payments by the November 15 deadline, you can still claim the full credit of up to $3,600 per child by filing your taxes next year.

See how the Child Tax Credit works for families like yours:

-

Jamie

- Occupation: Teacher

- Income: $55,000

- Filing Status: Head of Household (Single Parent)

- Dependents: 3 children over age 6

Jamie

Jamie filed a tax return this year claiming 3 children and will receive part of her payment now to help her pay for the expenses of raising her kids. She’ll receive the rest next spring.

- Total Child Tax Credit: increased to $9,000 from $6,000 thanks to the American Rescue Plan ($3,000 for each child over age 6).

- Receives $4,500 in 6 monthly installments of $750 between July and December.

- Receives $4,500 after filing tax return next year.

-

Sam & Lee

- Occupation: Bus Driver and Electrician

- Income: $100,000

- Filing Status: Married

- Dependents: 2 children under age 6

Sam & Lee

Sam & Lee filed a tax return this year claiming 2 children and will receive part of their payment now to help her pay for the expenses of raising their kids. They’ll receive the rest next spring.

- Total Child Tax Credit: increased to $7,200 from $4,000 thanks to the American Rescue Plan ($3,600 for each child under age 6).

- Receives $3,600 in 6 monthly installments of $600 between July and December.

- Receives $3,600 after filing tax return next year.

-

Alex & Casey

- Occupation: Lawyer and Hospital Administrator

- Income: $350,000

- Filing Status: Married

- Dependents: 2 children over age 6

Alex & Casey

Alex & Casey filed a tax return this year claiming 2 children and will receive part of their payment now to help them pay for the expenses of raising their kids.

They’ll receive the rest next spring.

They’ll receive the rest next spring.- Total Child Tax Credit: $4,000. Their credit did not increase because their income is too high ($2,000 for each child over age 6).

- Receives $2,000 in 6 monthly installments of $333 between July and December.

- Receives $2,000 after filing tax return next year.

-

Tim & Theresa

- Occupation: Home Health Aide and part-time Grocery Clerk

- Income: $24,000

- Filing Status: Do not file taxes; their income means they are not required to file

- Dependents: 1 child under age 6

Tim & Theresa

Tim and Theresa chose not to file a tax return as their income did not require them to do so. As a result, they did not receive payments automatically, but if they signed up by the November 15 deadline, they will receive part of their payment this year to help them pay for the expenses of raising their child. They’ll receive the rest next spring when they file taxes.

If Tim and Theresa did not sign up by the November 15 deadline, they can still claim the full Child Tax Credit by filing their taxes next year.

If Tim and Theresa did not sign up by the November 15 deadline, they can still claim the full Child Tax Credit by filing their taxes next year.- Total Child Tax Credit: increased to $3,600 from $1,400 thanks to the American Rescue Plan ($3,600 for their child under age 6). If they signed up by July:

- Received $1,800 in 6 monthly installments of $300 between July and December.

- Receives $1,800 next spring when they file taxes.

- Automatically enrolled for a third-round stimulus check of $4,200, and up to $4,700 by claiming the 2020 Recovery Rebate Credit.

Frequently Asked Questions about the Child Tax Credit:

Overview

Who is eligible for the Child Tax Credit?

Getting your payments

What if I didn’t file taxes last year or the year before?

Will this affect other benefits I receive?

Spread the word about these important benefits:

For more information, visit the IRS page on Child Tax Credit.

Download the Child Tax Credit explainer (PDF).

ZIP Code-level data on eligible non-filers is available from the Department of Treasury: PDF | XLSX

The Child Tax Credit Toolkit

Spread the Word

2022 Child Tax Credit: Definition, How to Claim

You’re our first priority.

Every time.

We believe everyone should be able to make financial decisions with confidence. And while our site doesn’t feature every company or financial product available on the market, we’re proud that the guidance we offer, the information we provide and the tools we create are objective, independent, straightforward — and free.

So how do we make money? Our partners compensate us. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners.

Here is a list of our partners.

For the 2022 tax year, taxpayers may be eligible for a credit of up to $2,000 — and $1,500 of that may be refundable.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

This article has been updated for the 2022 tax year.

The child tax credit is a federal tax benefit that plays an important role in providing financial support for American taxpayers with children. For the 2022 tax year, people with kids under the age of 17 may be eligible to claim a tax credit of up to $2,000 per qualifying dependent, and $1,500 of that credit may be refundable.

We’ll cover who qualifies, how to claim it and how much you might receive per child.

What is the child tax credit?

The child tax credit, commonly referred to as the CTC, is a tax credit available to taxpayers with dependent children under the age of 17. In order to claim the credit when you file your taxes, you have to prove to the IRS that you and your child meet specific criteria.

In order to claim the credit when you file your taxes, you have to prove to the IRS that you and your child meet specific criteria.

You’ll also need to show that your income falls beneath a certain threshold because the credit phases out in increments after a certain limit is hit. If your modified adjusted gross income exceeds the ceiling, the credit amount you get may be smaller, or you may be deemed ineligible altogether.

Who qualifies for the child tax credit?

Taxpayers can claim the child tax credit for the 2022 tax year when they file their tax returns in 2023. Determining your eligibility for the credit begins with understanding which children qualify and what other criteria you need to be mindful of.

Generally, there are seven “tests” you and your qualifying child need to pass.

Age: Your child must have been under the age of 17 at the end of 2022.

Relationship: The child you’re claiming must be your son, daughter, stepchild, foster child, brother, sister, half brother, half sister, stepbrother, stepsister or a descendant of any of those people (e.

g., a grandchild, niece or nephew).

g., a grandchild, niece or nephew).Dependent status: You must be able to properly claim the child as a dependent. The child also cannot file a joint tax return, unless they file it to claim a refund of withheld income taxes or estimated taxes paid.

Residency: The child you’re claiming must have lived with you for at least half the year (there are some exceptions to this rule).

Financial support: You must have provided at least half of the child’s support during the last year. In other words, if your qualified child financially supported themselves for more than six months, they’re likely considered not qualified.

Citizenship: Per the IRS, your child must be a "U.S. citizen, U.S. national or U.S. resident alien," and must hold a valid Social Security number.

Income: Parents or caregivers claiming the credit also typically can’t exceed certain income requirements. Depending on how much your income exceeds that threshold, the credit gets incrementally reduced until it is eliminated.

Did you know...

If your child or a relative you care for doesn't quite meet the criteria for the CTC but you are able to claim them as a dependent, you may be eligible for a $500 nonrefundable credit called the "credit for other dependents." Check the IRS website for more information.

How to calculate the child tax credit

For the 2022 tax year, the CTC is worth $2,000 per qualifying dependent child if your modified adjusted gross income is $400,000 or below (married filing jointly) or $200,000 or below (all other filers). If your MAGI exceeds those limits, your credit amount will be reduced by $50 for each $1,000 of income exceeding the threshold until it is eliminated.

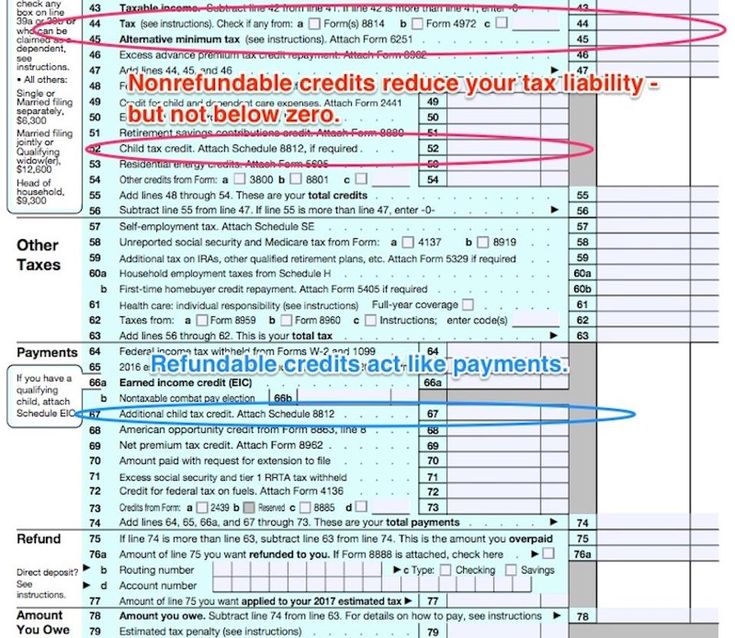

The CTC is also partially refundable; that is, it can reduce your tax bill on a dollar-for-dollar basis, and you might be able to apply for a tax refund of up to $1,500 for anything left over. This partially refundable portion is called the “additional child tax credit” by the IRS.

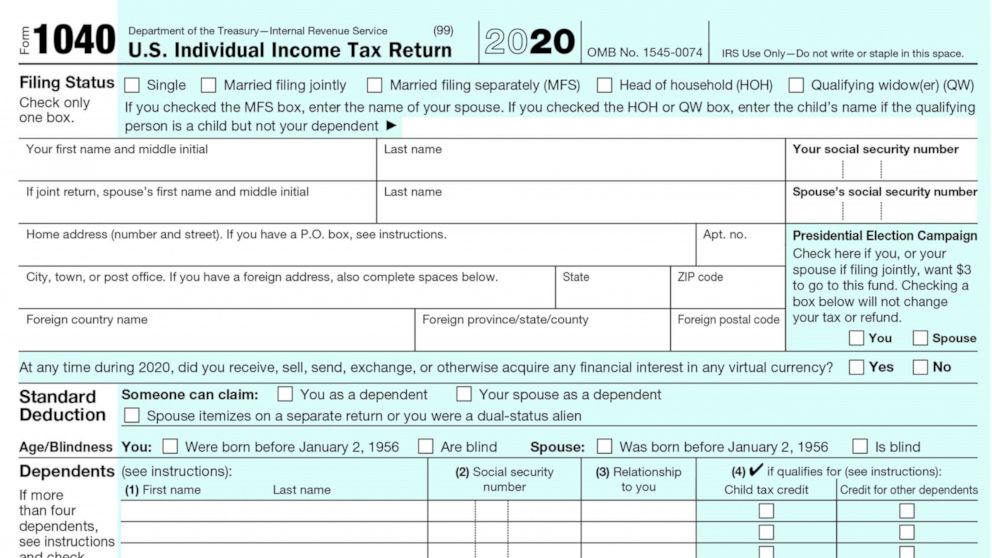

How to claim the credit

You can claim the child tax credit on your Form 1040 or 1040-SR. You’ll also need to fill out Schedule 8812 (“Credits for Qualifying Children and Other Dependents”), which is submitted alongside your 1040. This schedule will help you to figure your child tax credit amount, and if applicable, how much of the partial refund you may be able to claim.

Most quality tax software guides you through claiming the child tax credit with a series of interview questions, simplifying the process and even auto-filling the forms on your behalf. If your income falls below a certain threshold, you might also be able to get free tax software through IRS’ Free File.

A word of warning: In the eyes of the IRS, you’re ultimately responsible for all information you submit, even if someone else prepares your return.

🤓Nerdy Tip

If you applied for the additional child tax credit, by law the IRS cannot release your refund before mid-February.

Consequences of a CTC-related error

An error on your tax form can mean delays on your refund or on the CTC part of your refund. In some cases, it can also mean the IRS could deny the entire credit.

If the IRS denies your CTC claim:

You must pay back any CTC amount you’ve been paid in error, plus interest.

You might need to file Form 8862, "Information To Claim Certain Credits After Disallowance," before you can claim the CTC again.

If the IRS determines that your claim for the credit is erroneous, you may be on the hook for a penalty of up to 20% of the credit amount claimed.

State child tax credits

In addition to the federal child tax credit, a few states, including California, New York and Massachusetts, also offer their own state-level CTCs that you may be able to claim when filing your state return. Visit your state's department of taxation website for more details.

History of the CTC

Like other tax credits, the CTC has seen its share of changes throughout the years. In 2017, the Tax Cuts and Jobs Act, or TCJA, established specific parameters for claiming the credit that will be effective from the 2018 through 2025 tax years. However, the American Rescue Plan Act of 2021 (the coronavirus relief bill) temporarily modified the credit for the 2021 tax year, which has caused some confusion as to which changes are permanent.

Here's a brief timeline of its history.

1997: First introduced as a $500 nonrefundable credit by the Taxpayer Relief Act.

2001: Credit increased to $1,000 per dependent and made partially refundable by the Economic Growth and Tax Relief Reconciliation Act.

2017: The TCJA made several changes to the credit, effective from 2018 through 2025. This included increasing the credit ceiling to $2,000 per dependent, establishing a new income threshold to qualify and ensuring that the partially refundable portion of the credit gets adjusted for inflation each tax year.

2021: The American Rescue Plan Act made several temporary modifications to the credit for the 2021 tax year only. This included expanding the credit to a maximum of $3,600 per qualifying child, allowing 17-year-olds to qualify, and making the credit fully refundable. And for the first time in U.S. history, many taxpayers also received half of the credit as advance monthly payments from July through December 2021.

2022–2025: The 2021 ARPA enhancements ended, and the credit will revert back to the rules established by the TCJA — including the $2,000 cap for each qualifying child.

Frequently asked questions

1. Does the CTC include advanced payments this year?

The American Rescue Plan Act made several temporary modifications to the credit for tax year 2021, including issuing a set of advance payments from July through December 2021. This enhancement has not been carried over for this tax year as of this writing.

2. I had a baby in 2022. Am I eligible for the CTC?

Yes. You'll likely need to make sure your child has a Social Security number before you apply, though.

3. Is the child tax credit taxable?

No. It is a partially refundable tax credit. This means that it can lower your tax bill by the credit amount, and if you have no liability, you may be able to get a portion of the credit back in the form of a refund.

4. Is the child tax credit the same thing as the child and dependent care credit?

No. This is another type of tax benefit for taxpayers with children or qualifying dependents. It covers a percentage of expenses you made for care — such as day care, certain types of camp or babysitters — so that you can work or look for work. The IRS has more details here.

About the authors: Sabrina Parys is a content management specialist at NerdWallet. Read more

Tina Orem is NerdWallet's authority on taxes and small business. Her work has appeared in a variety of local and national outlets. Read more

Her work has appeared in a variety of local and national outlets. Read more

On a similar note...

Get more smart money moves – straight to your inbox

Sign up and we’ll send you Nerdy articles about the money topics that matter most to you along with other ways to help you get more from your money.

all about personal finance and consumer rights

All about personal finance and consumer rights. How to take advantage of the tax deduction if you get an education, pay for medical treatment or buy real estate. How to check debts on loans and fines. How to return a damaged product to the store or achieve a markdown.

Popular

-

All about tax deductions

-

How to get a tax deduction when buying an apartment

-

How to return or exchange an item in the store

-

How transport tax is calculated

-

How to pay VAT

-

How to return or exchange an item in the store

How to return defective goods to the store.

How to return an item purchased from an online store. Which items are non-returnable and non-exchangeable. How to obtain payment for the repair of low-quality goods

How to return an item purchased from an online store. Which items are non-returnable and non-exchangeable. How to obtain payment for the repair of low-quality goods -

How to check and pay your tax debt

How to check the accrued taxes. How to find out tax debt online by TIN. How to pay tax debts. How to apply for an installment plan for the payment of tax debt

-

How to get a tax deduction for education expenses

How to apply for a tax deduction for education expenses. Is it possible to return part of the taxes paid if I paid for the education of the child.

Is it possible to get a tax deduction if I paid for my studies at a driving school or courses

Is it possible to get a tax deduction if I paid for my studies at a driving school or courses -

How to get a tax deduction when buying an apartment

How to get a tax deduction when buying real estate. Is it possible to get a tax deduction for the repair of an apartment. How to get a tax deduction when buying an apartment on a mortgage

-

How to check loan debt

How to check loan debt. Where is credit history stored and how to challenge it. What threatens credit debt

-

How to pay VAT

What is personal income tax and who is obliged to pay it.

When do you need to file a self-declaration? How to fill out the 3-NDFL declaration correctly and pay income tax

When do you need to file a self-declaration? How to fill out the 3-NDFL declaration correctly and pay income tax -

How to file for child support

Who can apply for alimony and what documents are needed for this. Where to apply for alimony and how much each child is entitled to support

-

How to pay less for utility bills

Who can get a subsidy for utility bills, when you can not pay for them, and what services you can refuse

-

How to rent an apartment in Moscow

How to properly rent an apartment and conclude a lease, lease or sub-lease agreement.

How to pay taxes for renting out a property. When do I need to register an agreement with Rosreestr

How to pay taxes for renting out a property. When do I need to register an agreement with Rosreestr -

All about tax deductions

What are the tax deductions and how to apply for them. What part of the taxes paid can be returned. Who is eligible for tax deductions

-

How to check and pay a legal debt

How to check debts on the website of the Federal Bailiff Service. For what debts can deprive rights. For what debts they can not be released abroad. How to get a certificate of absence of judicial debts

-

How to get a standard tax deduction for a beneficiary

Who can get the standard tax deduction.

The amount of tax deductions for beneficiaries. What documents are needed to apply for a tax deduction for a beneficiary

The amount of tax deductions for beneficiaries. What documents are needed to apply for a tax deduction for a beneficiary -

How to get a tax deduction when selling property

How to get a tax deduction when selling an apartment. Is it possible to pay less taxes by selling a car. What documents are needed to receive a property tax deduction

-

How transport tax is calculated

How the transport tax is calculated. Who has the right not to pay transport tax. Do I need to report my car to the tax office on my own? How to calculate the amount of tax using a special calculator.

How to pay tax

How to pay tax -

How is personal property tax calculated?

How is the tax on property of individuals in Moscow calculated. Where can I find the current tax rates. Who is eligible for benefits. How to report your property to the tax office

how to use mat capital in 2022

Published: 06/25/2021 Updated: 23.09.2022

Content

-

•

Who can get uterus

-

•

Where you can spend maternity capital

-

•

How to extinguish the mortgage of matern

•

How to deposit maternity capital into a mortgage: a step-by-step guide

-

•

Methods of repayment of mortgages by maternal capital

-

•

Possible risks

-

•

Nuances

-

•

Conclusion

•

How to extinguish the mortgage

9000•

•

•

•

•

•

•

•

•

9000 •Allocation of shares

Cash assistance is given to spouses who have their first or second child after 2020. The subsidy is also provided for the birth of subsequent children, but only if the parents did not receive payment earlier.

The subsidy is also provided for the birth of subsequent children, but only if the parents did not receive payment earlier.

The amount of capital for the first child in 2022 is 524,500 ₽, and for the second — 168,600 ₽. If the first-born in the family was born before 2020, the amount of capital for the second child will be 693,100 ₽. The state support program is valid until 2026.

Maternal capital can be used for various purposes, including the improvement of living conditions. With the help of maternity capital, you can pay off an already issued mortgage. The subsidy can be used as a down payment on a mortgage loan.

Who can get maternity capital

-

•

families in which at least one of the spouses has Russian citizenship;

-

•

parents who adopted a second child or subsequent children after 2020;

-

•

parents whose child is a citizen of the Russian Federation.

Maternity capital is issued not for each child, but only once. At the same time, funds are transferred only in non-cash form - in the form of an electronic or paper certificate.

Where can maternity capital be spent? Maternity capital is also allowed to be used for other purposes:

-

•

as a down payment on a mortgage. Families with children have access to preferential mortgage lending programs. Alfa-Bank has an offer at a rate of 5.7% per annum;

-

•

to repay interest on a mortgage loan or to partially repay the body of the loan. Partial early repayment will help reduce the loan term or reduce the amount of monthly payments. As a result, the total overpayment on the transaction will decrease;

-

•

to pay off the outstanding debt. If the mortgage debt is less than or equal to the amount of maternity capital, borrowers will be able to completely close the debt with its help.

The presence of MSC gives the right to take advantage of preferential terms, but does not guarantee a mortgage loan. In order for a bank to approve a loan, you need to have a good credit history, a sufficient level of income and a steady income.

How to pay off a mortgage with maternity capital: features and conditions

Maternity capital may be used to pay the down payment, repay the principal debt and interest debt on a mortgage-backed housing loan or loan. The procedure for repayment of a mortgage loan is regulated by Art. 10 of the Federal Law No. 256. Among the basic requirements are the following:

-

•

the acquired property must be located on the territory of Russia;

-

•

in housing purchased with state support funds, it is necessary to allocate equal shares for spouses and minor children;

-

•

the purchased housing is registered in the ownership of the main borrower;

-

•

maternity capital can be used for the purchase, reconstruction of housing, the purchase of real estate under the DDU, as well as for the acquisition of individual housing plots;

-

•

a mortgage loan must be obtained from a bank, AIZhS (DOM.

RF) or a credit cooperative;

RF) or a credit cooperative; -

•

funds cannot be used to pay accrued penalties, fines or bank commissions. Matkapital is intended only for payment of the actual debt and / or accrued interest;

-

•

money is given out in a single amount, not in installments.

In order to invest maternity capital in repaying a home loan, it is not necessary to wait until the child is three years old. As a rule, a mortgage transaction must be coordinated with the creditor bank, as well as the Pension Fund of the Russian Federation.

How to deposit maternity capital into a mortgage: a step-by-step guide

To transfer maternity capital to a mortgage account, you must submit an application to the pension fund. Instruction:

Step 1: contacting the bank

First of all, you need to get a certificate from the bank for the Pension Fund stating that the borrower is applying for a mortgage (or has issued it earlier). The certificate indicates the number of the loan agreement, the personal data of the borrowers, the total amount of debt, bank details for transferring funds.

The certificate indicates the number of the loan agreement, the personal data of the borrowers, the total amount of debt, bank details for transferring funds.

Step 2: registration of the obligation

Next, draw up a notarial obligation. The document guarantees that the parent who received the MSC will allocate shares in the acquired housing to the children after the full repayment of the debt and removal of the encumbrance. The following documents are required to complete the obligation:

-

•

passports of all family members;

-

•

birth certificates for children under 14;

-

•

extract from the USRN;

-

•

mortgage agreement and maternity capital certificate;

-

•

sale and purchase agreement, DDU or assignment agreement.

Additionally, you need to make certified copies, since the original will remain in the PF, and the certificate will still be useful when distributing shares.

Step 3: Applying to the Pension Fund

Before paying the mortgage with maternity capital, the certificate holder submits an application to the Pension Fund of the Russian Federation. The document must indicate the type of expenses, as well as the amount of funds required. Attached to the application:

-

Passports of spouses, certificate of registration (or dissolution) of marriage.

-

Documents confirming the purchase of real estate, as well as confirming the ownership of the borrowers - DKP, DDU.

-

SNILS, original or duplicate of the certificate.

-

A copy of the loan agreement with the repayment schedule.

Certificate of the balance of the debt and interest on the date of application for a subsidy, mortgage.

Certificate of the balance of the debt and interest on the date of application for a subsidy, mortgage. -

A notarized commitment that the borrower undertakes to allocate shares to all family members.

-

Certificate indicating the account of the certificate holder.

-

Receipt confirming the transfer of funds to the real estate seller.

If the family plans to use the mother's capital for the construction (reconstruction) of a house, a building permit and documents for the land plot will be required.

How to submit documents:

The Pension Fund reviews the application within two weeks. The maximum review period is 30 days. If the fund makes a positive decision, the state support funds will be credited to the applicant's account in 10 days. After that, the bank will accept the money for early repayment of the mortgage.

Step 4: submitting an application to the bank

Next, the decision to repay the mortgage (loan body or interest) with family capital must be reported to the credit institution. It is advisable to do this before the due date of the mandatory payment. To deposit funds, borrowers submit to the bank an application, a certificate, as well as a certificate from the Pension Fund on the balance of funds in the account.

After the approval of the procedure, the money is transferred to the account of the creditor bank. Next, the bank will recalculate and send a new payment schedule. If the MSC funds were enough to fully repay the loan, the borrower needs to take a certificate of no debt. In the future, the encumbrance is removed from the real estate: the corresponding application is submitted to the Rosreestr.

Ways to repay a mortgage with maternity capital

State subsidy can be used as a down payment on a mortgage issued for:

-

•

purchase of an apartment on the secondary market or in a new building;

-

•

construction or reconstruction of a private house;

-

•

acquisition of a residential building, the degree of wear of which does not exceed 50%.

With MSC funds, you can close part of the principal debt or pay interest on the loan. With partial early repayment, you can reduce the amount of mandatory payments or shorten the loan period.

With MSC funds, you can close part of the principal debt or pay interest on the loan. With partial early repayment, you can reduce the amount of mandatory payments or shorten the loan period.

You should first choose a suitable bank. Alfa-Bank offers preferential lending programs, including those with the possibility of using maternity capital funds. A mortgage with maternity capital can be issued both on a general basis and on preferential terms: at a rate of 5.7% per annum.

When making the mother's capital as a first installment, it is advisable to add part of your own funds, since the PF transfers money within a month. When signing a loan agreement, the money will not be taken into account, and the bank will recalculate later.

Possible risks

There are some nuances in using maternity capital:

Possible risks

Features

Getting a tax deduction

According to the law, you can get a tax benefit only if the property was purchased with your own funds. There is no deduction from government subsidies. If the family made a deduction, and after that repaid part of the mortgage with maternity capital, then the amount received from these funds must be returned

There is no deduction from government subsidies. If the family made a deduction, and after that repaid part of the mortgage with maternity capital, then the amount received from these funds must be returned

Sale of real estate

When selling real estate purchased with the help of MSK, difficulties may arise. This is due to the fact that when applying for a mortgage, parents allocate shares to all children. The sale of shares of minor owners requires permission from the guardianship and guardianship authorities. Without a document, the transaction will be invalid

Mortgage refinancing

Not all banks are ready to refinance mortgage loans that were paid with MSC funds. The refinancing procedure provides for the transfer of debt from one creditor to another with simultaneous removal of the encumbrance and re-registration of the agreement. This situation potentially violates the rights of children who have shares in real estate

Terms of funds transfer

If the Pension Fund has made a positive decision, it will send a notification to the applicant within five days. Money upon application is transferred on average within 10 days. This is important to consider when applying to the bank. During the consideration of documents, interest is accrued on the standard terms specified in the loan agreement.

Money upon application is transferred on average within 10 days. This is important to consider when applying to the bank. During the consideration of documents, interest is accrued on the standard terms specified in the loan agreement.

Submitting an online application

You can register with the Pension Fund to apply and provide original documents through the public services portal. To do this, you need to have a verified account and log in to the site. Then:

-

•

select the "Services" tab and go to the "Family and Children" section;

-

•

open the “Maternal capital management” tab and select electronic receipt of the service;

-

•

click the "Get service" button and send the application for consideration.

In a few days, an invitation will come with an indication of the time of visiting the PF.

How to pay off a mortgage with maternity capital in Alfa-Bank

The instructions for repaying a mortgage using maternity capital at Alfa-Bank are as follows:

-

•

You can get a certificate for MSC, you can do it in electronic form;

-

•

submit an application and a standard package of documents, including a statement of the balance of available funds under the certificate;

-

•

execution of a mortgage loan transaction;

-

•

no later than 6 months after obtaining a mortgage loan, the borrower must submit an application for disposal of maternity capital at any branch of Alfa-Bank.

On average, the subsidy is credited to the account within 30 working days from the date of application. You can track changes in the balance of the debt on the website or in the mobile application.

Reasons for refusal

The right to use family capital funds to pay off a mortgage is established at the legislative level. According to Article 8 of the Federal Law No. 256, the reasons for refusal are:

-

•

loss of the right to receive state support - deprivation of parental rights, cancellation of adoption;

-

•

errors, inaccurate information in the submitted documents, provision of an incomplete set of documents;

-

•

non-compliance of the creditor bank with the requirements of the Pension Fund of the Russian Federation.

In addition, the Pension Fund will refuse an application for the purchase of housing recognized as emergency or subject to reconstruction.

Allocation of shares

After full repayment of the mortgage and removal of the encumbrance from the real estate, the certificate holder must fulfill the obligation to allocate shares within 6 months from the moment the loan is closed.

There is no clear provision in the law on what the shares should be. In practice, shares are distributed in proportion to what percentage of the total mortgage debt is repaid by the allocated funds. With the appearance of a third or subsequent child in the family, another share in real estate is allocated. Thus, there is a redistribution of shares.

Nuances

-

•

You can pay for a mortgage loan issued by one of the spouses before marriage registration with mother capital. Provided that the spouses filed an application with the FIU after they legalized the relationship;

-

•

other relatives of the spouses: parents, brothers, sisters cannot participate in the distribution of shares in real estate, since they are not considered members of the family of certificate holders;

-

•

adult children and spouse may refuse to allocate shares.