How much is one child on income tax

2022 Child Tax Credit: Requirements, How to Claim

You’re our first priority.

Every time.

We believe everyone should be able to make financial decisions with confidence. And while our site doesn’t feature every company or financial product available on the market, we’re proud that the guidance we offer, the information we provide and the tools we create are objective, independent, straightforward — and free.

So how do we make money? Our partners compensate us. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners.

Taxpayers may be eligible for a credit of up to $2,000 — and $1,500 of that may be refundable.

By

Sabrina Parys

Sabrina Parys

Content Management Specialist | Taxes, investing

Sabrina Parys is a content management specialist on the taxes and investing team. Her previous experience includes five years as a project manager, copy editor and associate editor in academic and educational publishing. Sabrina earned a master's degree in publishing at Portland State University.

Learn More

and

Tina Orem

Tina Orem

Senior Writer/Spokesperson | Small business, taxes

Tina Orem covers small business and taxes at NerdWallet. She has a degree in finance, as well as a master's degree in journalism and a Master of Business Administration. Her work has appeared in a variety of local and national media outlets. Email: <a href="mailto:[email protected]">[email protected]</a>.

Learn More

Edited by Arielle O'Shea

Arielle O'Shea

Lead Assigning Editor | Retirement planning, investment management, investment accounts

Arielle O’Shea leads the investing and taxes team at NerdWallet. She has covered personal finance and investing for 15 years, previously as a researcher and reporter for leading personal finance journalist and author Jean Chatzky. Arielle has appeared as a financial expert on the "Today" show, NBC News and ABC's "World News Tonight," and has been quoted in national publications including The New York Times, MarketWatch and Bloomberg News. Email: <a href="mailto:[email protected]">[email protected]</a>.

She has covered personal finance and investing for 15 years, previously as a researcher and reporter for leading personal finance journalist and author Jean Chatzky. Arielle has appeared as a financial expert on the "Today" show, NBC News and ABC's "World News Tonight," and has been quoted in national publications including The New York Times, MarketWatch and Bloomberg News. Email: <a href="mailto:[email protected]">[email protected]</a>.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

This article has been updated for the 2022 tax year.

The child tax credit is a federal tax benefit that plays an important role in providing financial support for American taxpayers with children. People with kids under the age of 17 may be eligible to claim a tax credit of up to $2,000 per qualifying dependent when they file their 2022 tax returns in 2023. $1,500 of that credit may be refundable

People with kids under the age of 17 may be eligible to claim a tax credit of up to $2,000 per qualifying dependent when they file their 2022 tax returns in 2023. $1,500 of that credit may be refundable

We’ll cover who qualifies, how to claim it and how much you might receive per child.

What is the child tax credit?

The child tax credit, commonly referred to as the CTC, is a tax credit available to taxpayers with dependent children under the age of 17. In order to claim the credit when you file your taxes, you have to prove to the IRS that you and your child meet specific criteria.

You’ll also need to show that your income falls beneath a certain threshold because the credit phases out in increments after a certain limit is hit. If your modified adjusted gross income exceeds the ceiling, the credit amount you get may be smaller, or you may be deemed ineligible altogether.

Who qualifies for the child tax credit?

Taxpayers can claim the child tax credit for the 2022 tax year when they file their tax returns in 2023. Generally, there are seven “tests” you and your qualifying child need to pass.

Generally, there are seven “tests” you and your qualifying child need to pass.

Age: Your child must have been under the age of 17 at the end of 2022.

Relationship: The child you’re claiming must be your son, daughter, stepchild, foster child, brother, sister, half brother, half sister, stepbrother, stepsister or a descendant of any of those people (e.g., a grandchild, niece or nephew).

Dependent status: You must be able to properly claim the child as a dependent. The child also cannot file a joint tax return, unless they file it to claim a refund of withheld income taxes or estimated taxes paid.

Residency: The child you’re claiming must have lived with you for at least half the year (there are some exceptions to this rule).

Financial support: You must have provided at least half of the child’s support during the last year. In other words, if your qualified child financially supported themselves for more than six months, they’re likely considered not qualified.

Citizenship: Per the IRS, your child must be a "U.S. citizen, U.S. national or U.S. resident alien," and must hold a valid Social Security number.

Income: Parents or caregivers claiming the credit also typically can’t exceed certain income requirements. Depending on how much your income exceeds that threshold, the credit gets incrementally reduced until it is eliminated.

Did you know...

If your child or a relative you care for doesn't quite meet the criteria for the CTC but you are able to claim them as a dependent, you may be eligible for a $500 nonrefundable credit called the "credit for other dependents." Check the IRS website for more information.

How to calculate the child tax credit

For the 2022 tax year, the CTC is worth $2,000 per qualifying dependent child if your modified adjusted gross income is $400,000 or below (married filing jointly) or $200,000 or below (all other filers). If your MAGI exceeds those limits, your credit amount will be reduced by $50 for each $1,000 of income exceeding the threshold until it is eliminated.

The CTC is also partially refundable; that is, it can reduce your tax bill on a dollar-for-dollar basis, and you might be able to apply for a tax refund of up to $1,500 for anything left over. This partially refundable portion is called the “additional child tax credit” by the IRS.

How to claim the credit

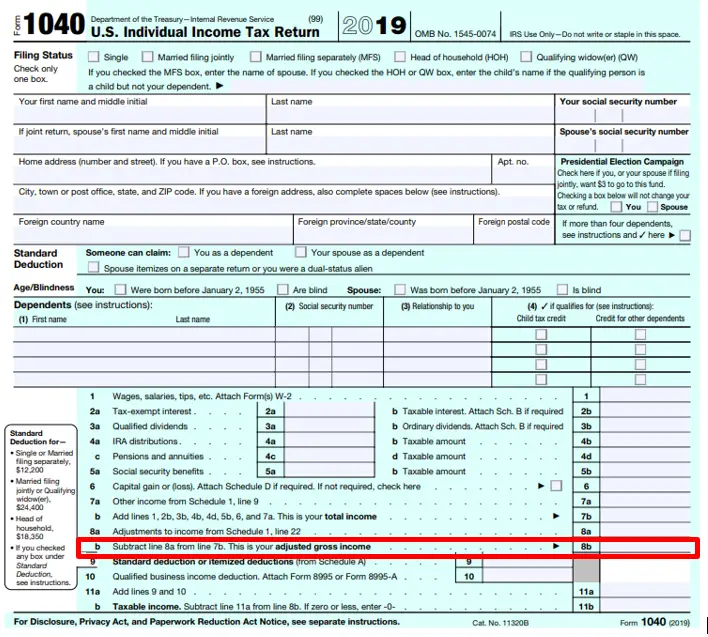

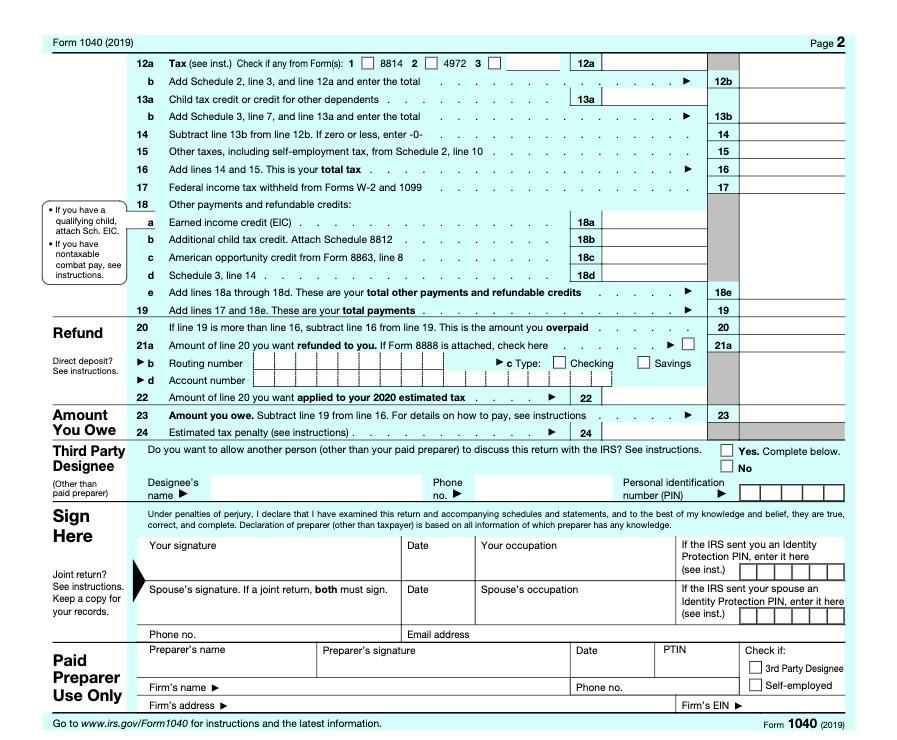

You can claim the child tax credit on your Form 1040 or 1040-SR. You’ll also need to fill out Schedule 8812 (“Credits for Qualifying Children and Other Dependents”), which is submitted alongside your 1040. This schedule will help you to figure your child tax credit amount, and if applicable, how much of the partial refund you may be able to claim.

Most quality tax software guides you through claiming the child tax credit with a series of interview questions, simplifying the process and even auto-filling the forms on your behalf. If your income falls below a certain threshold, you might also be able to get free tax software through IRS’ Free File.

🤓Nerdy Tip

If you applied for the additional child tax credit, by law the IRS cannot release your refund before mid-February.

Consequences of a CTC-related error

An error on your tax form can mean delays on your refund or on the child tax credit part of your refund. In some cases, it can also mean the IRS could deny the entire credit.

If the IRS denies your CTC claim:

You must pay back any CTC amount you’ve been paid in error, plus interest.

You might need to file Form 8862, "Information To Claim Certain Credits After Disallowance," before you can claim the CTC again.

If the IRS determines that your claim for the credit is erroneous, you may be on the hook for a penalty of up to 20% of the credit amount claimed.

State child tax credits

In addition to the federal child tax credit, a few states, including California, New York and Massachusetts, also offer their own state-level CTCs that you may be able to claim when filing your state return. Visit your state's department of taxation website for more details.

Visit your state's department of taxation website for more details.

History of the CTC

Like other tax credits, the CTC has seen its share of changes throughout the years. In 2017, the Tax Cuts and Jobs Act, or TCJA, established specific parameters for claiming the credit that will be effective from the 2018 through 2025 tax years. However, the American Rescue Plan Act of 2021 (the coronavirus relief bill) temporarily modified the credit for the 2021 tax year, which has caused some confusion as to which changes are permanent.

Here's a brief timeline of its history.

1997: First introduced as a $500 nonrefundable credit by the Taxpayer Relief Act.

2001: Credit increased to $1,000 per dependent and made partially refundable by the Economic Growth and Tax Relief Reconciliation Act.

2017: The TCJA made several changes to the credit, effective from 2018 through 2025. This included increasing the credit ceiling to $2,000 per dependent, establishing a new income threshold to qualify and ensuring that the partially refundable portion of the credit gets adjusted for inflation each tax year.

2021: The American Rescue Plan Act made several temporary modifications to the credit for the 2021 tax year only. This included expanding the credit to a maximum of $3,600 per qualifying child, allowing 17-year-olds to qualify, and making the credit fully refundable. And for the first time in U.S. history, many taxpayers also received half of the credit as advance monthly payments from July through December 2021.

2022–2025: The 2021 ARPA enhancements ended, and the credit will revert back to the rules established by the TCJA — including the $2,000 cap for each qualifying child.

Frequently asked questions

Does the child tax credit include advanced payments this year?

The American Rescue Plan Act made several temporary modifications to the credit for tax year 2021, including issuing a set of advance payments from July through December 2021. This enhancement has not been carried over for this tax year as of this writing.

Is the child tax credit taxable?

No. It is a partially refundable tax credit. This means that it can lower your tax bill by the credit amount, and if you have no liability, you may be able to get a portion of the credit back in the form of a refund.

Is the child tax credit the same thing as the child and dependent care credit?

No. This is another type of tax benefit for taxpayers with children or qualifying dependents. It covers a percentage of expenses you made for care — such as day care, certain types of camp or babysitters — so that you can work or look for work. The IRS has more details here.

I had a baby in 2022. Am I eligible to claim the child tax credit when I file in 2023?

If you also meet the other requirements, yes. You'll likely need to make sure your child has a Social Security number before you apply, though.

About the authors: Sabrina Parys is a content management specialist at NerdWallet. Read more

Tina Orem is NerdWallet's authority on taxes and small business. Her work has appeared in a variety of local and national outlets. Read more

Her work has appeared in a variety of local and national outlets. Read more

On a similar note...

Get more smart money moves – straight to your inbox

Sign up and we’ll send you Nerdy articles about the money topics that matter most to you along with other ways to help you get more from your money.

Tax Credits vs. Tax Deductions

You’re our first priority.

Every time.

We believe everyone should be able to make financial decisions with confidence. And while our site doesn’t feature every company or financial product available on the market, we’re proud that the guidance we offer, the information we provide and the tools we create are objective, independent, straightforward — and free.

So how do we make money? Our partners compensate us. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners.

Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners.

Tax deductions reduce your taxable income, but tax credits reduce your bill dollar for dollar.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

Tax credits and tax deductions may be the most satisfying part of preparing your tax return. Both reduce your tax bill, but in very different ways.

Tax credits directly reduce the amount of tax you owe, giving you a dollar-for-dollar reduction of your tax liability. A tax credit valued at $1,000, for instance, lowers your tax bill by the corresponding $1,000.

Tax deductions, on the other hand, reduce how much of your income is subject to taxes. Deductions lower your taxable income by the percentage of your highest federal income tax bracket. So if you fall into the 22% tax bracket, a $1,000 deduction saves you $220.

Would you rather have: | ||

A $10,000 tax deduction… | …or a $10,000 tax credit? | |

Your AGI | $100,000 | $100,000 |

Less: tax deduction | ($10,000) | |

Taxable income | $90,000 | $100,000 |

Tax rate* | ||

Calculated tax | $22,500 | $25,000 |

Less: tax credit | ($10,000) | |

Your tax bill | $22,500 | $15,000 |

The catch to tax credits

Some tax credits are nonrefundable.

That means that if you don’t owe a lot in taxes to begin with, you don’t get the full value if the credits take your tax bill below zero. In other words, a $600 tax bill combined with a $1,000 nonrefundable credit doesn’t get you a $400 tax refund check.

That means that if you don’t owe a lot in taxes to begin with, you don’t get the full value if the credits take your tax bill below zero. In other words, a $600 tax bill combined with a $1,000 nonrefundable credit doesn’t get you a $400 tax refund check.Some tax credits are refundable. If you qualify to take refundable tax credits — things such as the earned income tax credit or the child tax credit — the value of the credit goes beyond your tax liability and can result in a refund check.

The IRS lays out specific criteria you must meet to qualify for both nonrefundable and refundable credits.

A big decision about tax deductions

There are two types of tax-deduction strategies: taking the standard deduction or itemizing.

The standard deduction

The standard deduction is a one-size-fits-all reduction in the amount of your income that’s subject to tax.

You don’t have to do anything to qualify for the standard deduction or provide any documentation.

You don’t have to do anything to qualify for the standard deduction or provide any documentation.You can claim the standard deduction on Form 1040. The amount varies depending on your filing status.

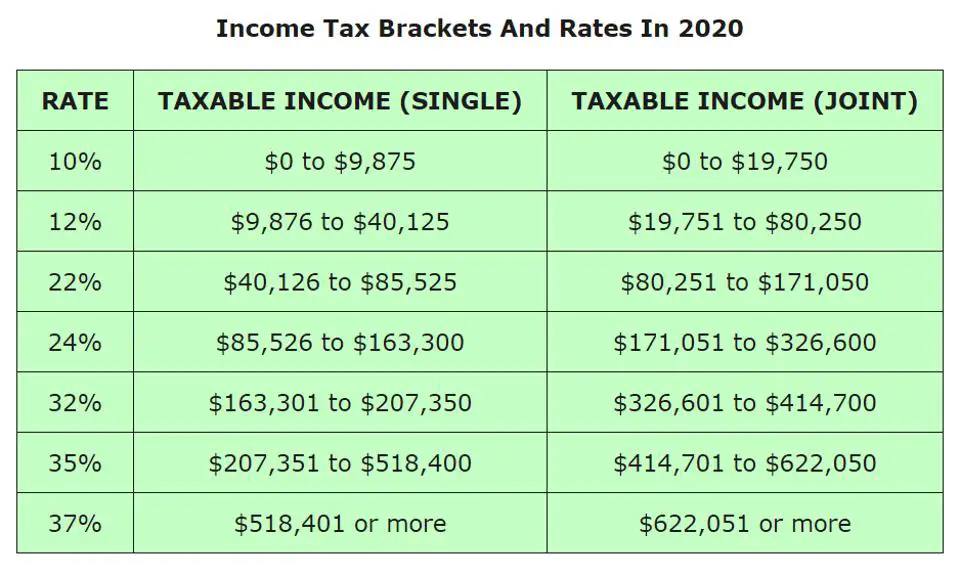

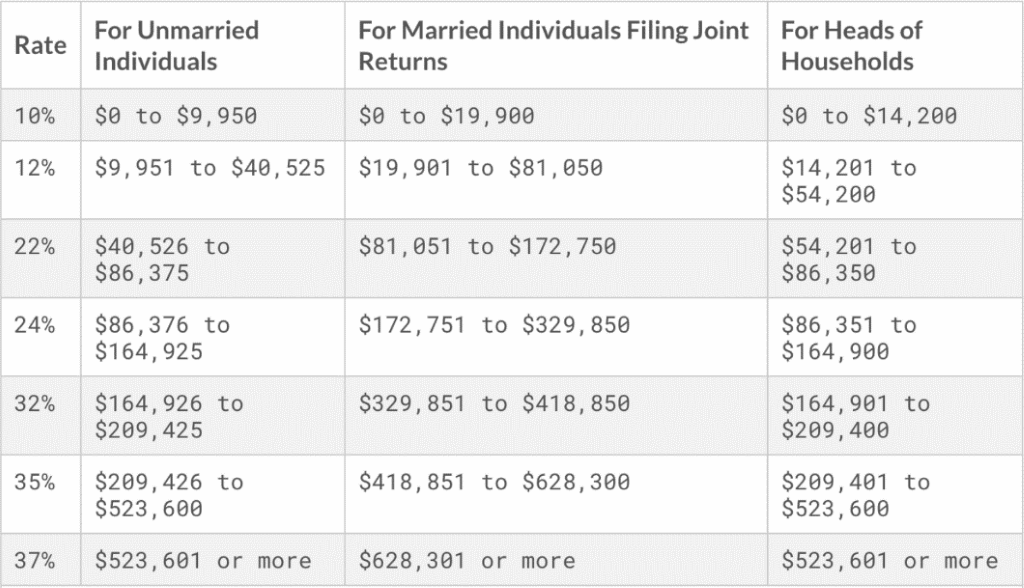

Filing status | 2021 tax year | 2022 tax year |

|---|---|---|

Single | $12,550 | $12,950 |

Married, filing jointly | $25,100 | $25,900 |

Married, filing separately | $12,550 | $12,950 |

Head of household | $18,800 | $19,400 |

Itemizing

Itemizing allows you to take advantage of deductions such as home mortgage interest, medical expenses or charitable donations. If together your itemized deductions exceed the value of the standard deduction, you'll want to itemize so you pay less tax.

:no_upscale()/cdn.vox-cdn.com/uploads/chorus_asset/file/13294673/lift_harris_bill.png) You'll need to use the regular Form 1040 and Schedule A.

You'll need to use the regular Form 1040 and Schedule A.Just as with tax credits, taking certain deductions requires meeting certain qualifications based on your filing status, current life events and the amount of your income that’s taxable. Be sure you meet IRS criteria to qualify for both tax credits and deductions.

Promotion: NerdWallet users get 25% off federal and state filing costs. | |

Promotion: NerdWallet users can save up to $15 on TurboTax. | |

|

On a similar note...

Get more smart money moves – straight to your inbox

Sign up and we’ll send you Nerdy articles about the money topics that matter most to you along with other ways to help you get more from your money.

Income tax - personal income tax [2022] ᐈ Personal income tax

Since 2011, the rates of personal income tax (PIT) are determined in Section IV of the Tax Code of Ukraine (TCU). Note that for the vast majority of fellow citizens and in the vast majority of cases, the personal income tax rate (or, as it is also called, income tax ), since 2016 is 18% .

The revision of the Tax Code of 2011 was not the ultimate truth, it changes periodically (and even more often than we would like). The latest changes came into effect on 29May 2020.

The latest changes came into effect on 29May 2020.

The changes that were made in May 2020 related to the sale of movable and immovable property. For the sale of the third (and subsequent) car during the year, you will have to pay not 5%, but 18%. When selling an object under construction - exemption from payment of 5%. In addition, the section "Pensions" is excluded.

| Type of income | Tax rate | Reference to the Tax Code (Section IV) | ||

|---|---|---|---|---|

| Income received in the form of wages, other incentive and compensation payments or other payments and remuneration paid to the payer in connection with labor relations and under civil law contracts | 18% | item 167.1 | ||

| 18% | p.165.1.26 | |||

| Income received by an individual from economic activity | 18% | p. 177.1 | ||

| Citizens' income received from independent professional activities | 18% | Clause 178.2 | ||

| Amounts of overspent funds received for a business trip or under a report, and not returned within the prescribed period | 18% | p. 170.9 | ||

| Income received from the provision of property to leasing, rent or sublease | 18% | .1 p. 170.1|||

| Investment income from the taxpayer with securities, discharge and corporate cadiac rights issued in forms other than securities (except for income from operations specified in clauses 165.1.2 and 165.1.40 of the TCU) | 18% | clause 170. 2 2 | ||

| life insurance in the event that the insured person reaches a certain age stipulated in the insurance contract, or the expiration of the contract | 18% | p. 170.8.2 | ||

| The redemption amount in case of early termination by the insured with a long -term life insurance contract | 18% | p.170.8.2 | ||

| The amount of funds from which the tax was not withheld paid to the contributor from his pension deposit or bank management fund participant's account in connection with the early termination of the pension deposit agreement, trust management, or non-state pension provision | 18% | clause 170.8.2 | ||

| Funds provided by the employer as assistance for burial (in the amount of excess over the value of the double subsistence minimum for an able-bodied person, multiplied by 1.4 and rounded to the nearest 10 UAH) | 18% | clause 165. 1.22 1.22 | ||

| Part of charitable assistance subject to taxation subject to the norms of clause 170.7 of the Tax Code | 18% | clause 170.7 | 18% | p. .h. for the rehabilitation of disabled people, the taxpayer and / or members of his family of the first degree of kinship, provided by his employer - the payer of income tax - free of charge or at a discount (in the amount of such a discount) once a year, (provided that the cost of the tour or discount is not exceeds 5 minimum wages) | is not taxed | , 165.1.35 |

| winnings, prizes, gifts | | |||

| winning or prize (except for winnings and prizes in the lottery) in favor of residents or non -residents | 18% 9003% 9003% 9003% 9003% 9003% . 167.1 167.1 | |||

| Win or prize in lottery | 18% | p.167.1 | ||

| Other winnings and prizes | 18% | pons 167.1 | ||

| Gifts (as well as prizes to winners and prizes competitions) if their value does not exceed 25% of the minimum wage, with the exception of cash payments in any amount | not taxed | clause 165.1.39 | ||

| Monetary winnings in sports competitions (except for remuneration to athletes - champions of Ukraine, prize-winners of international sports competitions, including athletes with disabilities, as defined in clause "b" clause 165.1 .1 TCU) | 18% | clause 167.1 | ||

| Funds, property, property or non-property rights, the cost of works, services donated to the taxpayer are taxed according to the rules for inheritance taxation (see section "Inheritance") nine0030 | 0% 5% 18% | p. 174.6 174.6 | ||

| percent | ||||

| percent for the current or deposit bank account | 18% | p.167.5.1 | or discount income on personalized savings (deposit) certificates | 18% | item 167.5.1 |

| Interest on deposit (deposit) in credit unions | 18% | |||

| Fee (percent) that is allocated to share membership fees of members of a credit union | 18% | item 167.5.1 | ||

| Income paid by the company managing the assets of a joint investment institution .167.5.1 | ||||

| Income from mortgage-backed securities (mortgage-backed bonds and certificates) | 18% | Clause 167.5.1 | ||

| Income in the form of interest (discount) received by their owner from bonds)0030 | 18% | p. 167.5.1 167.5.1 | ||

| Income from real estate fund certificates and income received as a result of redemption (redemption) of real estate fund certificates | 18% | p. | ||

| Interest and discount income accrued to individuals on any other grounds (except those listed in clause 170.4.1 of the Tax Code) | 18% | clause 170.4.3 | ||

| Dividends, royalties | 0018 | |||

| Dividends accrued in the form of shares (parts, shares) issued by a resident legal entity, provided that such accrual does not change the parts of the participation of all shareholders (owners) in the issuer's authorized capital, and as a result of which the issuer's authorized capital increases the total value of accrued dividends | is not subject to | clause 165.1.18 | ||

| Dividends on shares and corporate rights accrued by residents - payers of corporate income tax (except for income on shares and / or investment certificates paid by joint investment institutions ) nine0030 | 5% | clause 167. 5.2 5.2 | ||

| Dividends on shares and/or investment certificates and corporate rights accrued by non-residents, joint investment institutions, as well as business entities – not income tax payers | p. 167.5.4 | |||

| Royalti | 18% | p.170.3.1 | Real estate sale | |

| Income from the sale (exchange) not more than once during the reporting year of a residential building, apartment or part thereof, a room, a garden (country) house, as well as a land plot or an object of construction in progress, and provided that such property is owned by the payer tax over 3 years | not subject to tax | clause 172.1 | ||

Income from the sale during the reporting year of more than one of the real estate items specified in clause 172.1, as well as income from the sale of a real estate item not specified in clause 172. 1 172.1 1 172.1 | 5% | p. 172.2 | ||

| Sale of movable property | | |||

| income (exchange) of the object of movable property (except, see below) | 5% | 900|||

| Income from the sale (exchange) during the reporting year of one of the movable property (car, motorcycle, moped), not taxable (as an exception to the previous one) | not taxed | item 173.2 | ||

| Income from the sale (exchange) of the second object of movable property (car, motorcycle, moped) during the reporting year, is taxable | 5% | item 173.2 9022 Income from the sale (exchange) during the reporting year of the third (and subsequent) object of movable property (car, motorcycle, moped) is subject to taxation | 18% | p. 173.2 173.2 |

| Inheritance | | |||

| Value of property inherited by family members of the first degree of kinship | 0% | item 174.2.1 | 0% | Clause 174.2.1 |

| Monetary savings placed before 01/02/1992 in institutions of the USSR Savings Bank and USSR state insurance operating on the territory of Ukraine, or in government securities, and monetary savings of Ukrainian citizens placed to institutions of Oschadbank of Ukraine and the former Ukrgosstrakh during 1992–1994, the repayment of which did not take place | 0% | clause 174. 2.1 2.1 | ||

| The value of any object of inheritance received by heirs who are not members of the family of the testator of the first degree kinship | 5% | p.174.2.2 | ||

| The inheritance received by any heir from the testator is non -resident, and any object of the inheritance inherited by non -resident | 18% | p. 174.2.3 | ||

| Income of non-residents and foreign income | | |||

| Income originating in Ukraine, which are accrued or paid to non-residents | at rates determined for residents | item 170.10.1 | ||

| Foreign income | 18% | item 170.11.1 | ||

4 and rounded to the nearest UAH 10)

4 and rounded to the nearest UAH 10) On the financial portal Minfin.com.ua, it is easy to choose a loan online at a bank or microfinance organization. The catalog contains loans for everyone: cash loans in a bank, loans for people with a bad credit history, loans without refusal. You can compare rates for online microloans in different MFOs in Ukraine in the Indices section on Minfin.com.ua.

You can compare rates for online microloans in different MFOs in Ukraine in the Indices section on Minfin.com.ua.

The site collects and regularly updates deposit rates, which will help you compare and choose a deposit in dollars, euros or hryvnias. nine0011

In the "Banks" section, you can study all the information about the operating banks of Ukraine, as well as read or leave information about their products or services.

Personal income tax rates in Ukraine that were in force before:

- from 01/01/2019 to 05/28/2020

- from 01/01/2018 to 12/31/2018

- from 01/01/2017 to 12/31/2017

- from 07/01/2016 to 12/31/2016

- from 01/01/2016 to 06/30/2016

- from 01/01/2015 to 12/31/2015

- from 02.08.2014 to 31.12.2014

- See also:

- Minimum wage in Ukraine

Tax classes in Germany in 2022

What are the German tax classes. What are they for and how much tax depends on them.

When it comes to taxes, it usually comes to mind that they are very high in Germany. This is not true.

A significant part of deductions from income is not taxes, but social payments:

- health insurance,

- unemployment insurance contributions,

- from helplessness,

- to the pension fund.

Together fees take 20% of the salary. The structure of the German salary is discussed in detail in the article on gross and net pay in Germany.

In addition, the German Einkommensteuer income tax is levied on a progressive scale. Those who make good money pay more.

But that's not all. Germany has many different tax incentives. It is important to know how to use them. nine0011

Tax deductions depending on class

The main relaxations in Germany are related to tax classes - Steuerklasse. Thanks to the classes, German family workers receive relief from the monetary burden on their gross wages.

Classes are assigned to every person working in Germany, determining the annual value of the Steuerfreibetrag tax-free amount. Each option has its own deduction.

The tax class is entered on the Lohnsteuerkarte payroll card. nine0003 The card is not issued to the employee, but is an electronic record in the central database.

The employee receives an identification number in the database from the German tax office Finanzamt - IDN. When applying for a job, the IDN is reported to the new employer. The firm's HR department will access the electronic tax card and levy Lohnsteuer payroll tax on a monthly basis, taking into account the employee's tax class.

First tax class - Steuerklasse I

Assigned:

- by default in the first year of operation in Germany

- single, without family and children

- if the person is in the process of divorce and lives separately

- when the spouse lives abroad

- widowed workers in the second year after the death of a spouse

A foreigner who comes to Germany to work automatically receives first class until the family arrives and registers at the place of residence. nine0011

nine0011

The German tax system is complex and multi-tiered

The employee receives 9984€ exempt from taxation. The specified amount is deducted from the annual salary and taxes are paid from the rest. With monthly payments, the deduction is taken into account. At the end of the year, no recalculation is required due to the tax-exempt amount.

First class paying employees are not required to file a tax return in Germany. But he has the right to fill out the declaration voluntarily, which often leads to the return of part of the paid. nine0011

Second

Assigned to single parents if:

- father or mother lives with the child in the same dwelling

- fulfill the rules for receiving child benefit in Germany - Kindergeld

- parent is not married

- the employee really lives alone, without roommates

The class is not issued automatically, you must request a change by filling out the form. And the registration of the second adult in the apartment, on the contrary, automatically leads to a change to the first. nine0011

nine0011

To the tax-free 9984€ is added another 4008€ for heavy bachelor parental share. For the second and subsequent children, 240 € are added to the bonus.

If a single mother in 2022 with one child earns 13992€ per year, she does not pay salary tax. If more, the fee is paid on the amount exceeding the limit.

Read more about state benefits for single parents in Germany.

Third-Fourth-Fifth

Intended for family workers. nine0011

The third is beneficial when one of the spouses does not work at all or earns on MiniJob terms.

The base deduction for a holder of the third class is doubled. But another family member forfeits the tax-free amount by forcibly filing in the fifth. One of the couple gets the opportunity to write off €19968 from the tax base immediately.

If both work, you need to look at what is more profitable - to have a third class for one of the spouses or better if both remain at the base 9984€.

Then you can take the fourth. It looks like the first one, only intended for families. It only makes sense if both spouses work and earn about the same.

It looks like the first one, only intended for families. It only makes sense if both spouses work and earn about the same.

The fourth also allows you to share the total family tax break disproportionately. For example, a husband takes half of his wife's deduction.

The fifth is assigned to the spouse of the one who chose the third. The tax is collected from the entire amount of the annual salary.

Sixth

In case a person works in several jobs. On one of the jobs of choice, one of the five classes listed above is entered in the tax card, and on others, the sixth is automatically assigned. nine0011

Does not contain any tax-free amounts at all. This is the most disadvantageous class.

Explanations and hints

Filing a tax return through a Russian-speaking lawyer

Tax lawyer Evgeny Shevtsov will fill out and submit an income tax return in Germany, taking into account immigration nuances. An approximate estimate of the amount of the return is free! Pass

QUESTIONNAIRE

- Each employee has the right to change class once a year.