How much is child tax benefit 2023

The Child Tax Credit | The White House

To search this site, enter a search termThe Child Tax Credit in the American Rescue Plan provides the largest Child Tax Credit ever and historic relief to the most working families ever – and as of July 15th, most families are automatically receiving monthly payments of $250 or $300 per child without having to take any action. The Child Tax Credit will help all families succeed.

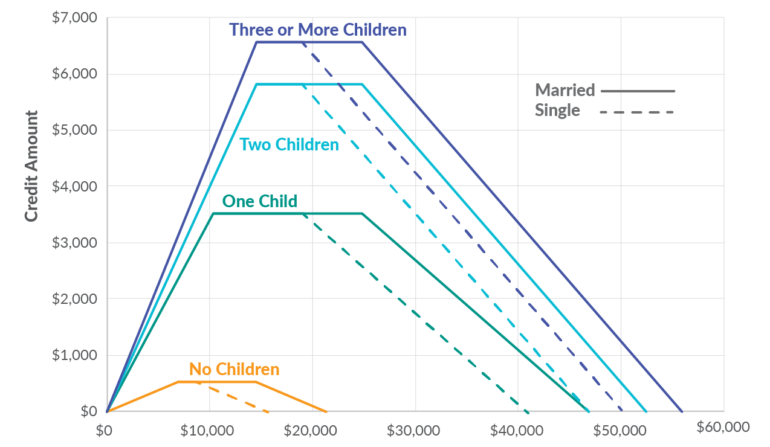

The American Rescue Plan increased the Child Tax Credit from $2,000 per child to $3,000 per child for children over the age of six and from $2,000 to $3,600 for children under the age of six, and raised the age limit from 16 to 17. All working families will get the full credit if they make up to $150,000 for a couple or $112,500 for a family with a single parent (also called Head of Household).

Major tax relief for nearly

all working families:

$3,000 to $3,600 per child for nearly all working families

The Child Tax Credit in the American Rescue Plan provides the largest child tax credit ever and historic relief to the most working families ever.

Automatic monthly payments for nearly all working families

If you’ve filed tax returns for 2019 or 2020, or if you signed up to receive a stimulus check from the Internal Revenue Service, you will get this tax relief automatically. You do not need to sign up or take any action.

President Biden’s Build Back Better agenda calls for extending this tax relief for years and years

The new Child Tax Credit enacted in the American Rescue Plan is only for 2021. That is why President Biden strongly believes that we should extend the new Child Tax Credit for years and years to come. That’s what he proposes in his Build Back Better Agenda.

Easy sign up for low-income families to reduce child poverty

If you don’t make enough to be required to file taxes, you can still get benefits.

The Administration collaborated with a non-profit, Code for America, who created a non-filer sign-up tool that is easy to use on a mobile phone and also available in Spanish. The deadline to sign up for monthly Child Tax Credit payments this year was November 15. If you are eligible for the Child Tax Credit but did not sign up for monthly payments by the November 15 deadline, you can still claim the full credit of up to $3,600 per child by filing your taxes next year.

The deadline to sign up for monthly Child Tax Credit payments this year was November 15. If you are eligible for the Child Tax Credit but did not sign up for monthly payments by the November 15 deadline, you can still claim the full credit of up to $3,600 per child by filing your taxes next year.

See how the Child Tax Credit works for families like yours:

-

Jamie

- Occupation: Teacher

- Income: $55,000

- Filing Status: Head of Household (Single Parent)

- Dependents: 3 children over age 6

Jamie

Jamie filed a tax return this year claiming 3 children and will receive part of her payment now to help her pay for the expenses of raising her kids. She’ll receive the rest next spring.

- Total Child Tax Credit: increased to $9,000 from $6,000 thanks to the American Rescue Plan ($3,000 for each child over age 6).

- Receives $4,500 in 6 monthly installments of $750 between July and December.

- Receives $4,500 after filing tax return next year.

-

Sam & Lee

- Occupation: Bus Driver and Electrician

- Income: $100,000

- Filing Status: Married

- Dependents: 2 children under age 6

Sam & Lee

Sam & Lee filed a tax return this year claiming 2 children and will receive part of their payment now to help her pay for the expenses of raising their kids. They’ll receive the rest next spring.

- Total Child Tax Credit: increased to $7,200 from $4,000 thanks to the American Rescue Plan ($3,600 for each child under age 6).

- Receives $3,600 in 6 monthly installments of $600 between July and December.

- Receives $3,600 after filing tax return next year.

-

Alex & Casey

- Occupation: Lawyer and Hospital Administrator

- Income: $350,000

- Filing Status: Married

- Dependents: 2 children over age 6

Alex & Casey

Alex & Casey filed a tax return this year claiming 2 children and will receive part of their payment now to help them pay for the expenses of raising their kids.

They’ll receive the rest next spring.

They’ll receive the rest next spring.- Total Child Tax Credit: $4,000. Their credit did not increase because their income is too high ($2,000 for each child over age 6).

- Receives $2,000 in 6 monthly installments of $333 between July and December.

- Receives $2,000 after filing tax return next year.

-

Tim & Theresa

- Occupation: Home Health Aide and part-time Grocery Clerk

- Income: $24,000

- Filing Status: Do not file taxes; their income means they are not required to file

- Dependents: 1 child under age 6

Tim & Theresa

Tim and Theresa chose not to file a tax return as their income did not require them to do so. As a result, they did not receive payments automatically, but if they signed up by the November 15 deadline, they will receive part of their payment this year to help them pay for the expenses of raising their child. They’ll receive the rest next spring when they file taxes.

If Tim and Theresa did not sign up by the November 15 deadline, they can still claim the full Child Tax Credit by filing their taxes next year.

If Tim and Theresa did not sign up by the November 15 deadline, they can still claim the full Child Tax Credit by filing their taxes next year.- Total Child Tax Credit: increased to $3,600 from $1,400 thanks to the American Rescue Plan ($3,600 for their child under age 6). If they signed up by July:

- Received $1,800 in 6 monthly installments of $300 between July and December.

- Receives $1,800 next spring when they file taxes.

- Automatically enrolled for a third-round stimulus check of $4,200, and up to $4,700 by claiming the 2020 Recovery Rebate Credit.

Frequently Asked Questions about the Child Tax Credit:

Overview

Who is eligible for the Child Tax Credit?

Getting your payments

What if I didn’t file taxes last year or the year before?

Will this affect other benefits I receive?

Spread the word about these important benefits:

For more information, visit the IRS page on Child Tax Credit.

Download the Child Tax Credit explainer (PDF).

ZIP Code-level data on eligible non-filers is available from the Department of Treasury: PDF | XLSX

The Child Tax Credit Toolkit

Spread the Word

Your First Look at 2023 Tax Brackets, Deductions, and Credits (3)

The US Bureau of Labor Statistics reported that the consumer price index increased just 0.1% for August after no change in July. However, inflation remains a concern because over the last 12 months, the index rose 8.3% before seasonal adjustment. And those rates could impact your 2023 tax picture.

The CPI measures the cost of goods and services in urban areas—in other words, your cost of living. It’s the most widely used measure of inflation since, as prices go up, the purchasing power of your dollar goes down. This is important information for taxpayers because the Tax Code provides for mandatory annual adjustments to certain tax items based on inflation.

(For more on inflation and the CPI, including a look at how the chained CPI works, check out this previous article.)

Bloomberg Tax’s projected US tax rates forecast that inflation-adjusted amounts in the tax code will increase by roughly 7.1% from 2022, more than double last year’s increase of 3%. What will inflation mean for your 2023 tax picture? “We predict that inflation-adjusted amounts in the tax code will increase significantly in 2023 compared to prior years due to the economic environment,” said Heather Rothman, vice president for Analysis & Content at Bloomberg Tax.

Here’s how that translates into dollars.

2023 Standard Deduction

For one, taxpayers will see a bump in the standard deductions. Since the doubling of the deduction due to tax reform, today, nearly 90% of taxpayers file using the standard deduction.

Married taxpayers were entitled to a standard deduction of $25,900 in 2022—that number is expected to jump to $27,700 in 2023./cdn0.vox-cdn.com/uploads/chorus_asset/file/6461621/graphic.0.png) Single and married individuals filing separately will see the standard deduction rise to $13,850, up from $12,950 in 2022. Heads of households will also see a boost to $20,800, up from $19,400 in 2022.

Single and married individuals filing separately will see the standard deduction rise to $13,850, up from $12,950 in 2022. Heads of households will also see a boost to $20,800, up from $19,400 in 2022.

The additional standard deduction for blind people and senior citizens will be $1,500 for married individuals and $1,850 for singles and heads of household in 2023.

Bloomberg also predicts that the standard deduction for taxpayers who may be claimed as a dependent by another taxpayer will be the greater of $1,250 or the sum of $400 plus the individual’s earned income.

2023 Tax Brackets

Tax brackets are also expanding. You can take advantage of these early numbers now. As Rothman noted, “Taxpayers and advisers can use our projections to begin their 2023 tax planning before the IRS publishes the official 2023 inflation-adjusted amounts later this year.”

Here’s how those are expected to look.

Individual Taxpayers

Married Taxpayers Filing Jointly

Married Taxpayers Filing Separately

Heads of Household

Capital Gains

As with income tax rates, the actual capital gains rates don’t change from year to year, but the brackets will widen in 2023. Short-term capital gains rates—for assets held less than a year—are the same as your income tax rates. But favorable long-term capital gain rates are dependent on your taxable income. Generally, the higher your income, the higher the rate.

Short-term capital gains rates—for assets held less than a year—are the same as your income tax rates. But favorable long-term capital gain rates are dependent on your taxable income. Generally, the higher your income, the higher the rate.

Here are the projected maximum zero rate and projected maximum 15% rate amounts for 2023:

Child Tax Credit

For the tax year 2021, the child tax credit amount increased from $2,000 to $3,600 for qualifying children under age 6, and $3,000 for other qualifying children under age 18. The entire amount was also refundable. However, the enhanced version of the credit disappeared in 2022—a version of the child tax credit remains in place for 2022 and 2023.

The 2023 credit amount will remain at the original $2,000 per qualifying child since it is not adjusted for inflation. However, the maximum refundable portion of the credit for a qualifying child is adjusted for inflation and is expected to be $1,600 in 2023.

Federal Estate & Gift Tax

Federal estate and gift tax numbers are moving, too. For 2023, the unified credit amount used to calculate the personal exemption will bump to $12,920,000 (or $25,840,000 for married couples). The annual exclusion for gifts is also expected to move up $1,000 to $17,000 in 2023.

For 2023, the unified credit amount used to calculate the personal exemption will bump to $12,920,000 (or $25,840,000 for married couples). The annual exclusion for gifts is also expected to move up $1,000 to $17,000 in 2023.

(For more on how the federal estate and gift tax system works, check out this previous article.)

What It Means for 2023

Wider tax brackets and increased exemptions and credits typically mean lower tax bills for most taxpayers, which is a good thing. But remember that this isn’t a bone being tossed to voters; it’s a statutory increase due to inflation.

And keep in mind that these are projections for the tax year 2023, beginning Jan. 1, 2023—the numbers you’ll use to prepare your tax return in 2024. These are not the tax rates and other numbers for 2022 that you’ll use to prepare your tax return in 2023.

Finally, remember that these are just projections. The IRS will publish the official tax brackets and other tax numbers for 2023 later this year—typically in October—and we’ll share those when available.

The 2023 tax projections are just one of the features available from Bloomberg Tax. The full report with additional projections is available for free here.

This is a regular column from Kelly Phillips Erb, the Taxgirl. Erb offers commentary on the latest in tax news, tax law, and tax policy. Look for Erb’s column every week from Bloomberg Tax and follow her on Twitter at @taxgirl.

Types of family benefits | Sotsiaalkindlustusamet

You are here

Home Children, families Applicants for family benefits Types of family benefits

If a child is born dead or die within 70 days

Parents have the right to birth benefit and parental compensation if the child is born dead or die in within 70 days.

Childbirth allowance

One of the parents is also entitled to childbirth allowance in case of stillbirth from the 22nd week of pregnancy. The allowance is one-time, in the amount of 320 euros. The right to receive childbirth allowance arises on the day the child is born.

The allowance is one-time, in the amount of 320 euros. The right to receive childbirth allowance arises on the day the child is born.

Parental benefit

If the mother works and is entitled to compensation for temporary disability

From April 1, 2022, a working mother is entitled to maternity leave and parental benefit to the mother for 100 consecutive calendar days starting from the 22nd week of pregnancy if the child is stillborn or dies within 70 calendar days. During this period, the mother is covered by health insurance.

If a mother started exercising her right to mother's parental benefit before the child was stillborn, she is entitled to mother's parental benefit and maternity leave for a total of 100 calendar days. For example, if a mother took maternity leave 70 calendar days before the birth of a child and started exercising her right to parental compensation to the mother after the birth of the child. dead, she is entitled to an additional 30 calendar days of maternity leave and parental benefit, for a total of 100 calendar days. If a mother took leave, for example, 30 calendar days before the birth, she is entitled to another 70 calendar days of maternity leave and parental compensation to the mother after the stillbirth of the child, for a total duration of 100 calendar days.

If a mother took leave, for example, 30 calendar days before the birth, she is entitled to another 70 calendar days of maternity leave and parental compensation to the mother after the stillbirth of the child, for a total duration of 100 calendar days.

An exception is also made here for mothers who, by the day of the child's death, have already used the mother's parental benefit in the amount of more than 70 calendar days. In this case, the mother is entitled to the mother's parental benefit additionally within 30 consecutive calendar days from the day following the day of the child's death. This means that no matter how many days the mother managed to use the mother's parental benefit by the day of the child's death, 30 calendar days of parental leave and parental benefit are guaranteed from the day of the child's death.

If the child dies at the time when the mother has managed to start using the already distributed parental benefit, the mother is re-registered as a recipient of the mother's parental benefit.

If the mother is not working

From April 1, 2022, a non-working mother is entitled to receive mother's parental benefit within 30 consecutive calendar days from the day following the day of the child's death, i.e. parental benefit cannot be received distributed by day over a long period of time, but if desired, you must use all 30 days in a row. During this period, the mother is covered by health insurance.

Fathers

From April 1, 2022, the father is entitled to paternity leave and father's parental benefit for 30 consecutive calendar days after the death of the child, regardless of whether the father used the right to paternity leave and father's parental benefit before the estimated date of birth of the child or before the death of the child. Father's parental benefit cannot be received on a daily basis over a long period of time, but if desired, all 30 days in a row must be used. In the case of fathers, there is no difference between granting and paying parental benefit, regardless of whether the father is working or not.

In order to receive family benefits, parents do not need to contact us and apply themselves. The Department of Social Insurance automatically obtains stillbirth information by exchanging data between the health information system and the social protection information system so that it is also possible to proactively offer family benefits to bereaved parents.

Additional parental paternity benefit is a type of benefit paid to fathers to enable them to take a greater part in the upbringing of their children. For working fathers, this is also accompanied by a 30-day leave from the employer.

For how long is compensation paid and for how long should it be scheduled?

You can receive additional parental benefit for a father for a total of 30 days, and not necessarily in a row (that is, the benefit can be received in installments). Supplemental parental benefit to the father can be received both during the period when the mother receives the parental allowance or the birth allowance (30 days before the expected date of birth of the child), and later.

The father is entitled to additional parental benefit until the child reaches the age of 3 or until the father receives regular parental benefit. Paternity leave cannot be separated from the receipt of compensation. If the father wishes to receive regular parental benefit without receiving additional parental benefit but does not notify us of the waiver of paternity leave, the Social Insurance Board will not be able to grant parental benefit until the father confirms his wish to waive paternity leave or use his. To fully waive paternity leave, you must submit an application to us.

Employment during paternity leave

While on paternity leave, the father must take a break from work at all his employers. The period of vacation use is entered in the Employment Register. During paternity leave, the father should not work and receive income! The principle of regular parental benefit does not apply, so the amount of parental benefit is not reduced when a maximum of half of the compensation has been received.

In accordance with the Law on Employment Contracts, an employer may refuse to grant leave if the notice of the desire to receive it is less than 14 days and for a period of less than 7 calendar days. Supplementary parental benefit to the father within the meaning of the Employment Contracts Act is a normal rest period, therefore, being on paternity leave does not adversely affect the calculation of annual leave and these days are considered working days when determining annual leave. Like being on vacation, parental leave does not reduce seniority.

Non-working fathers (including also self-employed persons (FIE) or representatives of the so-called liberal professions (e.g. notaries, bailiffs, sworn translators, auditors, bankrupt bailiffs), as well as persons working on the basis of a contract assignments and work contracts, etc. under the law of obligations, or members of the governing body of a legal entity) also receive additional parental benefit to the father for 30 calendar days. It can be used at any appropriate time from 30 days before the child's due date until the child reaches 3 years of age. The father can decide for himself whether he wants to receive the compensation in full at one time or in installments.

How to apply?

Be sure to talk to your child's mother and, if you have an employment relationship, also to your employer before applying. It must be borne in mind that the employer may refuse to grant a vacation of less than 7 days if you notify him less than 14 days in advance. If the employer agrees, there are no restrictions on our part - you can go on vacation from any day.

The application for additional parental benefit is made through the self-service environment. If you wish to take advantage of the leave until the birth of the child, you must indicate the personal code of the child's mother and the expected date of his birth. After the baby is born, you will find a pre-filled offer in the self-service environment. If you are unable to use the self-service environment, please contact us at [email protected].

If you are registered in the Employment Register as a person with a valid employment relationship, you will need to provide your employer's email address. You should also include the email address of the mother of the child. The self-service system will send them a notice of your leave application and put it on hold for 5 days. You don't need to do anything else.

The employer and the child's mother have 5 working days to tell us if they disagree with your leave application. If your employer or the child's mother does not submit their objections, the system will automatically enter a leave note in the Employment Register after 5 working days.

We will calculate the amount of your compensation and pay it to you at the beginning of the next month (the payout date is the 8th of each month).

How is paternity leave calculated?

Additional parental benefit to the father is calculated according to the same rules as regular parental benefit.

To calculate the benefit, we first subtract the 9 full calendar months prior to the birth of the child (i. e. the average length of pregnancy, whether the child was born on time, premature or postterm) and calculate the parental benefit based on income for the previous 12 calendar months. If the father takes a vacation in installments over several months, the average income for those calendar months is divided by the number of days in the month and then multiplied by the number of days the benefit is received.

The amount of compensation depends on the amount of social tax paid on the income received. Since the income is calculated based on the social tax paid during the 12 months of the reporting period, the amount based on the reporting period may differ from the exact income received at that time, so it is worth paying attention to the social tax paid during this period. You can read more about how parental benefits are calculated here. You can also use the parental benefit calculator (informative).

The minimum rate of parental benefit is the minimum wage rate of the previous calendar year in effect on 1 January (584 euros in 2022). The maximum amount of parental benefit is three times the average salary in Estonia calculated on the basis of the law for the previous year (4043.07 euros in 2022).

Example 1: During the period taken as the basis for the calculation, the father earned 1,500 euros per month. He went on paternity leave from January 14, 2021 to February 13, 2021, thus being on paternity leave for 30 consecutive days. Consequently, he was on parental leave for 17 days in January and 13 days in February. In January, the amount of his additional parental benefit amounted to (1500/31×17) 822.58 euros, in February - (1500/28×13) 696.43 euros.

Example 2: During the period taken as the basis for the calculation, the father earned 1200 euros per month. He took one week of paternity leave in January 2021, two weeks in February and the remaining 9 days in March. Thus, the amount of his additional parental benefit amounted to (1200/31×7) 270.97 euros in January, (1200/28×14) 600 euros in February and (1200/31×9) 348. 39 euros in March .

39 euros in March .

Other things to remember:

If several children were born in a family after 1 July 2020 at short intervals, then the right to 30 days of paternity leave and / or additional parental benefit to the father arises in connection with each child. Compensation / leave for each child should be used at different times - leave cannot be received at one time for all children, nor can multiple compensation be received in one period.

Twins are subject to one period, regardless of the number of twins.

If the family wants the father to receive both regular parental allowance and additional parental benefit to the father in succession, the first 30 days are always considered to be the period of additional parental benefit to the father. The father can start receiving regular parental allowance from the day when the child is at least 70 days old and the mother's maternity sheet is closed.

If you are on sick leave, it is recommended that you interrupt your paternity leave by notifying the Social Insurance Board as soon as possible. If you interrupt your paternity leave, the unused days are kept by you and can be used after your sick leave is closed.

If you interrupt your paternity leave, the unused days are kept by you and can be used after your sick leave is closed.

Starting on September 1, 2019 no longer assigned a child care fee

- due to children who were born on September 1, 2019, , , child care fee is no longer charged for a newborn baby or any other child growing up in the family . The state will gradually link the available funds with the new parental benefit system in the period 2020-2022.

- For all families where a child is born no later than August 31, 2019, we assign and pay a child care fee on the previous basis.

- Also for those who have already been assigned a childcare allowance as of August 31, 2019, we will continue to pay benefits .

We will continue paying the child care allowance until it ends, but no later than August 31, 2024.

At the same time, only one parent in the family is entitled to child care allowance (after the end of receiving parental benefit), if the family grows:

- child under 3 years old – EUR 38.36 per month for each child under 3 years old.

In addition, we pay a lower childcare allowance for children aged 3 to 8 if:

- from 3 to 8 years - 19.18 euros per month also for a child aged 3 to 8 years;

- There are 3 or more children in the family receiving child benefit – EUR 19.18 per month for each child aged 3 to 8 years.

If your child turns 8 in first grade, we will pay child care until the end of first grade, which is August 31st. If the child turns 8 in the second grade, or if the child is not in school, we will pay Child Care Allowance until the end of the month in which the child's birthday is.

Being on parental leave and receiving childcare allowance may be someone else instead of the child's parent. However, there is a rule that the amount of child care allowance paid to such a person cannot exceed 115.08 euros per month in total.

Example . The family has three children: aged 2 years, 3 years and 6 years. For a 2-year-old child, a child care allowance is paid in the amount of 38.36 euros per month. For a 3- and 6-year-old child, child care allowance is paid under the condition that in a family with three or more children, all children under the age of 8 will receive child care allowance. The amount of the child care allowance paid for both a 3-year-old and a 6-year-old child is 19,18 euros per child.

In total, the child care allowance is paid to the family in the amount of 38.36 + 19.18 + 19.18 = 76.72 euros per month.

In addition, such a family is paid a child allowance for each child, which is 60 euros for the first and second child, and 100 euros for the third child, for a total of 220 euros per month. Thus, the family receives child allowance and child care allowance totaling 296.72 euros per month .

Thus, the family receives child allowance and child care allowance totaling 296.72 euros per month .

The right to receive child care allowance arises after the end of receipt of parental benefit . However, we still recommend that you apply for child care allowance or agree to receive it as soon as you submit your initial application for family benefits. In this way, after the end of the payment of the parental benefit, we will be able to immediately begin the payment of the child care allowance.

However, keep in mind that if one of the parents leaves his job for parental leave, he is also entitled to the childcare allowance. Parental leave can be obtained from the employer.

The state pays social tax for the recipient of the child care allowance, and thus health insurance is provided by the state to the parent to whom we pay the child care allowance! You can read more about health insurance HERE.

Parental benefit and child care allowance are not paid simultaneously to the same family. This means that if we pay parental benefit for one child, during this period we suspend the payment of childcare allowance for all children growing up in the family.

This means that if we pay parental benefit for one child, during this period we suspend the payment of childcare allowance for all children growing up in the family.

Also, for the time you are already receiving maternity benefit or adoption allowance, we will not pay child care allowance for that child. Child care benefits received for other children are not affected by these benefits.

Methodology for accounting for the annual tax return » PITax.pl

▪ 8 stycznia 2020 r. ▪ Zaktualizowano: 13 grudnia 2020. ▪ Autor: Redakcja PITax.pl

Spis treści

- Annual tax return accounting method

- What is the tax amount?

- Tax calculation method

- What benefits can be deducted from the annual tax?

- When and how to pay tax?

- When and how to get a tax refund?

Methodology for accounting for the annual tax return

There are three options for calculating PIT-37 or PIT-36:

-

Only for yourself (individually),

-

For yourself and your spouse (together with your spouse),

-

As a single parent.

Spouses can calculate bills together if:

-

Were married during the entire previous year (since January 1),

-

During the entire previous year, there was a property community between them,

Nobody from spouses did not manage the department is covered by a one-time, unified tax or tax card. -

A citizen of Ukraine has a Polish tax residence.

The co-settlement option also applies to income tax settlement with a deceased spouse, i.e. when we were married before the start of the tax year and our spouse died during the tax year, or we remained married during the tax year and our spouse died after a tax year before filing a tax return. In this situation, we can also present a joint settlement.

| Attention! If one of the spouses is from Ukraine and does not have a Polish tax residence, then there is no possibility of a joint settlement, in which case two separate tax returns must be filed. |

For example, like a family with one parent, a taxpayer who is raising children who are:

They receive a social pension or care allowance, regardless of the children's income.

They are under 25 and still studying or studying and in the reporting year they did not receive an income (taxable under the tax scale or taxed at 19%) higher than PLN 3089 (this income does not include pensions).

A citizen of Ukraine who has a Polish tax residence can pay as a single parent, even if the child is in Ukraine or was born before the taxpayer received Polish tax residence.

Paying taxes together with a spouse or as a parent is more beneficial than an individual settlement because then the tax is calculated on a smaller amount.

What is the tax amount?

There are three types of taxation. Tax rates depend on the type of income.

-

Taxation under the tax scale 17.75%, 32%, on general terms - income from work, orders, pensions, economic activity, unregistered activity, from abroad, minor children and others (PIT-36, PIT- 37).

The amount of tax reduction in PIT calculations for 2019 is:

1) 1 420 PLN - for the tax base not exceeding 8 000 PLN,

2) for the calculation of tax and PL00 8) over PLN 13,000: PLN 1,420 minus the amount calculated according to the formula: PLN 871.70 × (tax base - PLN 8,000) ÷ PLN 5,000.

3) for tax calculation above PLN 13,000 and not more than PLN 85,528 – PLN 548.30

4) based on tax calculation exceeding PLN 85,528 and not exceeding PLN 127,000 – PLN 548.30 minus the amount calculated according to the formula: PLN 548.30 × (tax calculation basis – PLN 85 528) ÷ PLN 41 472

5) for a tax base exceeding PLN 127,000 – tax reduction without amount.

Persons under the age of 26 whose earnings under an employment contract and commission did not exceed PLN 35,636.67 in 2019 are exempt from paying tax.

Tax calculation method

1. Turnover – tax-deductible expenses = income.

2. Income - social security contributions - deductions from income = taxable amount.

3. Calculate the tax specified in the field above on the tax base.

4. Taxable amount - health insurance premiums - tax credits = tax debt (tax liability).

If the tax due is higher than the advance payments received by the employer, we have tax to pay, and if it is higher, we have an overpayment of tax and the office is required to return the excess amount.

C) Flat tax rate 19% - income from business activities, sale of real estate, cryptocurrencies, securities (PIT-36L, PIT-38, PIT-39)

For the above sources of income, the tax is 19% of income.

In this case, deductible taxes include all expenses related to generating income. There are no statutory amounts here. It is important that expenses are related to income. For example, such expenses include:

-

For the sale of real estate - expenses that increase the value of real estate incurred during its possession (for example, expenses for finishing the premises, inheritance and gift taxes paid, expenses for press advertising, commissions for agencies, etc.)

-

For capital income, cryptocurrencies are, for example, expenses for the purchase of securities sold, brokerage commissions, etc.).

-

For business - purchase of goods, office expenses, accounting services.

-

Detailed instructions for completing Forms PIT-36, 36L, 38, 39 can be found on the website; https://pomoc. pitax. pl/

C) Flat-rate taxation - for business transactions for which this method of taxation was chosen at the time of creation or during the conduct of business (PIT-28).

The amount of tax depends on the type of business. Their amount is specified in the Law on Flat Income Tax on Certain Income Received by Individuals. The amount of tax is from 2 to 20% of the income received. The tax base is income. For a flat rate, the tax is not taxable.

What benefits can be deducted from the annual tax?

Benefits reduce the tax paid or increase the tax refund. Therefore, it is worth including them in your annual tax return. We distinguish between tax deductions and income. The right to deduct benefits on your annual tax return is not determined by citizenship.

benefits deducted from income in 2020 (income tax for 2019) include:

-

Donations

-

In public interest,

-

-

For blood donation purposes, i.

e. blood or plasma donation.

e. blood or plasma donation. -

For educational and professional training purposes

-

Rehabilitation assistance - expenses incurred by or for the rehabilitation of a disabled person to facilitate the daily functioning of such a person.

-

Internet benefit - for people who settled this benefit for the first time or settled it a year ago.

-

Individual Retirement Account Benefit (IKZE) - payments to an individual retirement account to save funds for retirement,

-

Refund of unjustifiably collected benefits that previously increased taxable income, such as the return of ZUS.

-

Development assistance - expenses incurred for research and development in development.

-

Interest rate cuts - for people who started qualifying apartment investments during benefit years, housing costs incurred during the benefit period may be deducted.

-

Child benefit – family benefit for parents raising children.

-

Housing allowance – deduction of expenses for systematic savings in a savings account based on an agreement entered into before 2002.

-

Benefit for foreigners - assistance to people who worked abroad and paid taxes there.

for religious purposes, for religious purposes, for religious purposes, for religious purposes for religious purposes, for religious purposes for religious purposes, for religious purposes, for religious purposes for religious purposes for religious purposes for religious purposes for religious purposes for religious purposes for religious purposes for religious purposes for religious purposes for religious purposes for religious purposes for religious purposes for religious purposes,

9014 church care,| Donations must be made by organizations located in the countries of the European Union or the European Economic Area. Therefore, a donation made to an institution located in Ukraine cannot be deducted. |

Tax benefits also include:

| Important! A parent who earns income in Poland has the right to deduct family allowance even if he is not a Polish citizen. In addition, the child is not required to be in Poland. The fact of payment of income in Poland gives the right to the payment of child benefit. |

When and how to pay tax?

The tax arising from the annual tax return (line "Must be paid") must be paid by the end of April (by the end of February in the case of PIT-28). You do not need to pay tax at the same time as filing/sending your PIT to the tax office. PIT can be sent, for example, in March, and the tax is paid no later than 30.04.

The tax can be paid in cash (at the office cash desk, by bank transfer) or in non-cash form, for example, from a bank account via the Internet.

The tax must be paid using a micro tax account. Its number can be found on the government website podatki.gov.pl or obtained from any tax office by indicating the NIP or PESEL number.

If a foreigner is still waiting for a decision on granting PESEL, he can pay value added tax from the tax micro-account of the tax office in accordance with the list of tax bank account numbers of the National Tax Administration (effective from January 1, 2020).